Reader Bruce Hall comments on this post showing the implications of a short horizon probit model of recession likelihood.

Perhaps I didn’t remember correctly, but during the Biden Administration when there were ongoing discussions about whether or not there had been a recession or there was a recession on the way, you had made an observation that it seemed some people were cheering on a recession. My comments was that it seemed some people were doing that now. It wasn’t pointed at you. Sorry if it seemed that way.

This picture summarizes one reason why I didn’t think a recession was imminent in 2022:

Figure 1: U.Michigan economic sentiment (blue, left scale), 1yr-Fed funds spread, % (brown, right scale). NBER defined peak-to-trough recession dates shaded gray. Conjectured 2022H1 recession dates shaded light green. Source: U.Michigan, Treasury, Fed, NBER, and author’s calculations.

For the sight impaired, the 1yr-Fed funds spread (highlighted by Miller (2019) as the highest AUROC spread at 1-2 months horizon) was strongly positive, while the March 2025 spread is negative. While the sentiment indicator is higher now than in 2022, but not statistically significantly so (it’s about half a standard deviation difference).

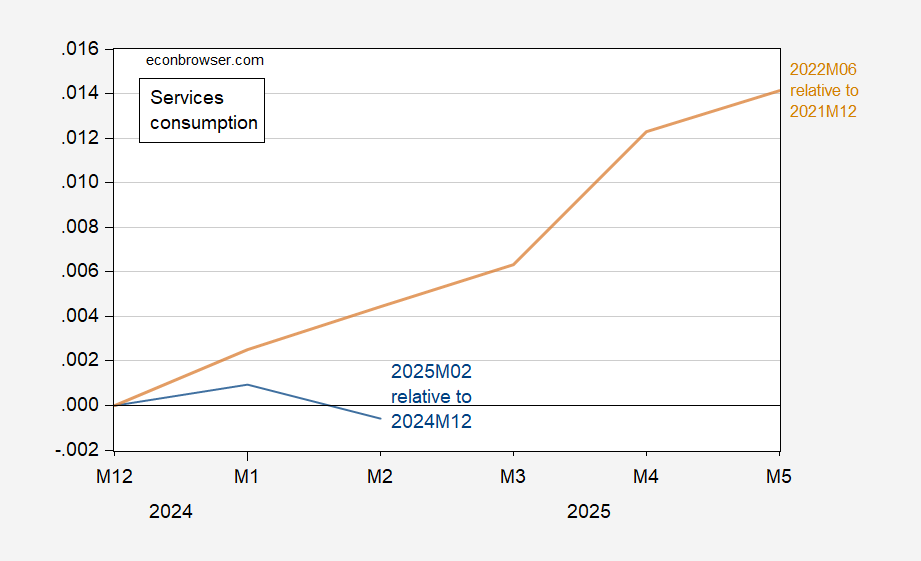

Moreover, in addition to employment growing strongly through 2022H1 (see Figure 1 of this post), services consumption (which should be the variable most strongly determined by the Hall-permanent income hypothesis view) was also growing strongly. That’s quite different than in 2025M02.

Figure 2: Services consumption relative to 2024M12 (blue), and relative to 2021M12 (tan). Source: BEA, and author’s calculations.