Before buying a home in the midst of a pandemic, you need to understand several things that are going on in the mortgage industry. This information is vital if you want to make the best purchase possible with the information available.

I’ve kept in touch with the mortgage lender representative who refinanced my previous home in 2019. He works for one of the top five largest banks in the country and is a top 20% producer in his department. In other words, he knows exactly what is going on in the mortgage market from the inside.

The housing market is heating up for a number of reasons:

- Mortgage rates have hit all-time lows so affordability is up

- Months of pent-up demand due to shelter-in-place and confidence is returning

- The realization that having a home is more valuable because more time is spent at home

- The desire to have a nicer home given we are spending more time at home

- The desire to invest in a relatively more stable asset class

- Overall supply is still suppressed

If you doubt my assertion that real estate is heating up, mortgage-purchase applications reached an 11-year high in May 2020. I’m pretty sure the index will continue to be high in June and beyond. The intent to buy property is very strong.

What You Need To Know In The Mortgage Market

Despite the strong rebound in mortgage-purchase applications, real estate investors should not make a sweeping generalization that all property segments will surge higher.

Here’s what’s going on in the mortgage market according to my lending officer. We spoke for about an hour.

Liquidity (Profitability) Concerns: A growing percentage of people are not paying their mortgages and banks are uncertain if and when payments will resume. As a result, his bank is only lending to the most financially fit customers.

Stricter Lending Standards: Due to liquidity (profitability) concerns, banks have significantly tightened lending standards. Here are some of the increased lending standards he mentioned to me:

- Temporarily stopped allowing for cash-out refinances

- No longer fully counting RSU values when calculating how much a person can borrow

- No longer including Schedule E income (rental income) when calculating how much a person can borrow – big shocker

- No longer approving Home Equity Lines Of Credit (HELOC)

- Minimum downpayment is 20%

- Raised minimum credit score to qualify for a mortgage to 680

In other words, lending standards are as strict as it gets.

Forced PPP Lending: Due to the origination fees that banks collect on government-guaranteed PPP money, I would have thought that all banks would be ecstatic about the PPP loan program. However, my mortgage lender expressed concern that PPP lending was crowding out other lending activities. He said his bank was also concerned it would have to record losses for a year before the government reimburses the bank for the PPP loans.

Jumbo Loans Are More Difficult To Obtain: For 2020, the Federal Housing Finance Agency raised the maximum conforming loan limit for a single-family property from $484,350 to $510,400. In other words, a loan of $510,401 is considered a jumbo loan. The conforming loan limit in San Francisco, California, and some other counties is $765,600 for a single-family home or condo.

It is easier to obtain a conforming loan because banks are able to sell the mortgage to government-backed Freddie Mac and Fannie Mae. Jumbo loans cannot be sold off to these institutions. When a bank sells a mortgage, its attendant risk also gets transferred, which means the bank can now originate more mortgages.

However, my lender said something I have never heard previously. He said that with new regulation, after selling a mortgage to Fannie Mae, if the borrower was late on even a single payment or is in forbearance, his bank would be required to not only buy back the entire mortgage, but also pay an 11-point penalty (11%). An 11-point penalty is equivalent to a $77,000 penalty on a $700,000 loan.

Jumbo loans cannot be sold to Fannie Mae or Freddie Mac. They can be sold in the private secondary market. However, due to more regulations, my lender said his bank is keeping most of the jumbo loans on its books. Therefore, banks are being extra stringent when evaluating borrowers who seek jumbo loans.

Small Business Owners Are Getting More Scrutinized: He’s noticed that small business owners are getting penalized disproportionately more than W2 employees because his lender is concerned small businesses will not recover. In contrast, there continues to be only a routine concern about the W2 employee loan applicant potentially losing his or her job.

During underwriting, if a small business got a PPP loan, it could be seen as a red flag regarding the viability of the small business. This is an interesting stance because you can also make the argument that a small business has a greater chance of surviving because it has received a PPP loan.

But most lenders also use the same logic and say that a rental or vacation property is riskier and therefore requires a larger down payment and a higher interest rate because the lender is assuming the borrower requires rental income to be able to afford the property. Whereas, some people like me take the view that any rental income is simply a bonus.

How A Tighter Mortgage Industry Will Affect Housing

When you put all this information together, it’s logical to make the assumption that the housing market should slow down. So long as tighter lending standards are in place, there will be less capital available to buy property.

However, there is overwhelming demand to purchase property due to the confluence of reasons I stated in my introduction. Further, there are still plenty of folks with 20%+ down, high credit scores, and low debt-to-income ratios that will qualify for a mortgage.

Therefore, as of now, demand for homes that can be purchased with a conforming mortgage ($510,400 – $765,600) is relatively strong. Assuming a 80% loan-to-value ratio, there is strength in the $638,000 – $957,000 price segment and below.

The lower the loan-to-value ratio (higher the down payment), the higher the priced home a person can buy. For example, a person can afford a $2,765,600 home using a conforming loan if he puts down $2,000,001, or a for a 72.32% downpayment, the loan-to-value ratio is 27.68%.

As a buyer borrows more and moves on to a jumbo loan, this is where borrowing gets more difficult.

Example Of A Jumbo Loan Rejection

My lender gave me an example of a borrower couple with a combined $630,000 income who got rejected for a $1.6 million jumbo loan. Usually, getting a mortgage that is less than 3X your gross income shouldn’t be a problem. However, in this scenario, the borrower owned four homes.

All four homes had mortgages that totaled roughly $2.3 million. Despite the mortgages, the homes were all cash flow positive. However, because my lender excluded Schedule E (rental income) in its underwriting consideration, the borrow wasn’t able to include over $150,000 in rental income.

If the lender had done so, however, the borrower’s total income would have been over $700,000. Lenders traditionally only consider ~70% of rental income to be conservative.

As a result of the tightened lending standards, the borrower’s purchase application was rejected by my lender. However, my lender referred the rejected applicant to one of his friends at another top-five largest bank. A month later, the applicant got approved.

Jumbo loans are happening, but they are just getting more difficult to obtain and longer to close. You just have to shop around.

As a result, if you want to find value in the housing market, it’s best to look for homes in your neighborhood that traditionally would require a jumbo loan.

In San Francisco, a lot of dual-income earning couples who have been saving for 10+ years can come up with up to a $500,000 down payment and buy up to a $2,500,000 home nowadays. Many of these tech firms are paying 22-year-old college graduates $100,000 – $140,000 in total compensation a year.

We’ve also gone through a 10+-year bull market in the S&P 500 and NASDAQ. Therefore, I’m no longer surprised when a 30-35-year-old tells me he or she is looking to buy a $2 – $2.5 million home.

But once you get above $2.5 million, it gets a little more difficult for many of these dual-income earning couples. They not only need a larger down payment, but they may also need a larger income to support a higher mortgage. Hence, there is an increased need to obtain a jumbo loan.

However, if you are able to buy property above ~$2.5 million in San Francisco, you’ll be able to get relatively better deals.

It’s up to you to find that higher price point in your city where there are more deals to be had. Looking for property near your city’s median home price is currently a tough proposition.

Don’t Get Too Excited About Your Mortgage Preapproval

There’s one last thing I want to leave you with. If you get preapproved for a jumbo mortgage in this tight lending environment, it’s easy to feel good. Pat yourself on the back for a nanosecond.

However, I recommend you turn your feeling of triumph into CAUTION. Getting preapproved for a mortgage today is like being part of a small team of soldiers landing on the beaches of your enemy.

Your combat skills and artillery may be top notch, but your enemy will still wipe you out simply because it outnumbers you 10-to-1. To win the war, you would rather have 100X more people on your side with fighter jets and warships.

If you hope for the property market to continue going up, you’d rather have everybody qualified for a mortgage instead of only a small few.

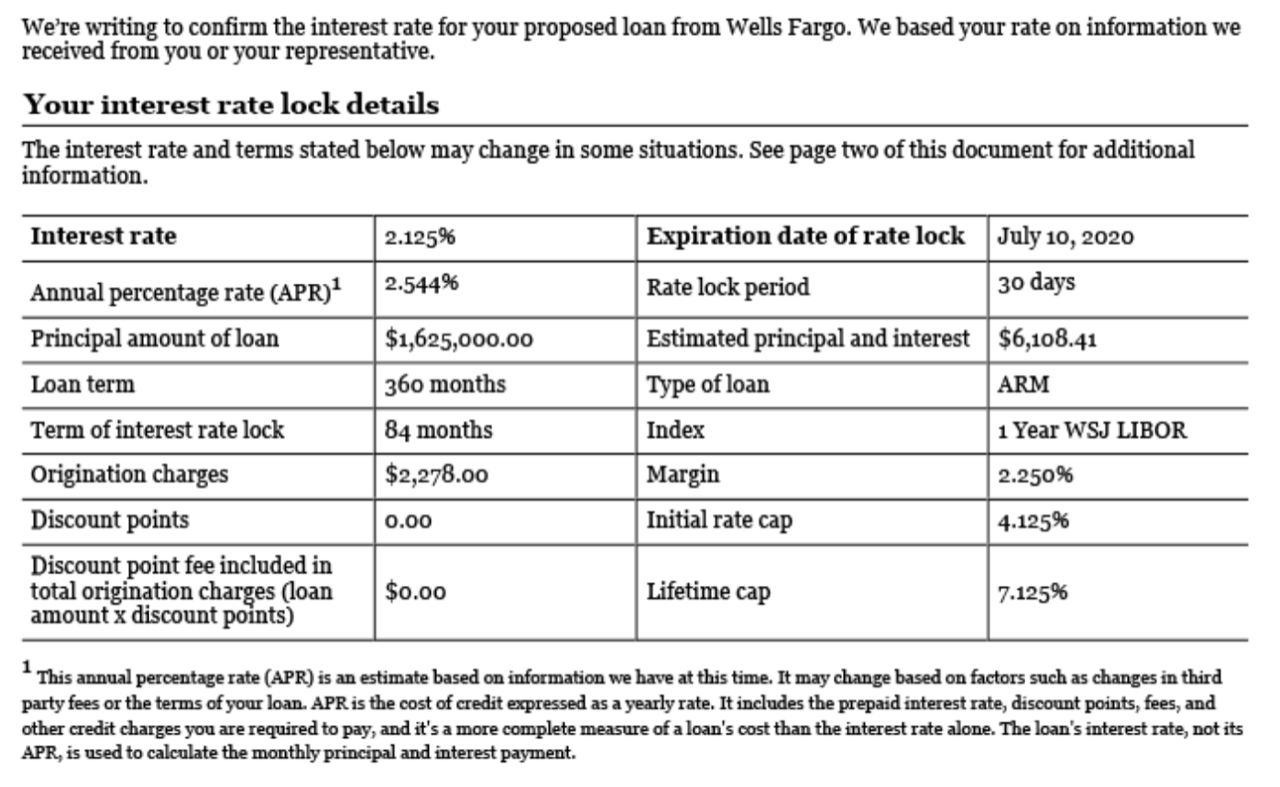

I’ve been preapproved for a 7/1 jumbo ARM at 2.125%. I’ve found an off-market house with panoramic ocean views that I want to buy. My goal is to buy as many panoramic ocean view homes in San Francisco for under $1,000/sqft as I can comfortably afford because I believe they are significantly undervalued today.

This home I have found would have sold for ~10% more pre-pandemic than what I can buy it for today. As a result, I’ve locked in my rate. All that’s left is trying to get an even better price.

But I’m concerned about moving forward because I don’t know when the banks will return to their normal lending standards. Everybody is depending on the government’s and the Federal Reserve’s continued support to keep the economy from falling into the abyss. Let’s hope enhanced unemployment benefits will be extended, more stimulus checks will be paid, and a third round of PPP loans comes to fruition.

A 2.125% rate for a 7/1 ARM jumbo is absurdly low. Yes, I am benefitting by 0.375% due to relationship pricing (I have assets with the lender). But still, even 2.5% for a 7/1 ARM jumbo is a great rate. My current rate is so low that it’s pushing me to want to buy another property.

If you’ve ever had the good fortune to purchase an engagement ring, it’s a similar feeling. Once you buy one, it burns a hole in your pocket where you just have to propose ASAP instead of waiting for the most opportune moment. YOLO, right?

But this type of thinking is dangerous thinking.

Nobody should buy a property just because they have locked in an ultra-low mortgage rate. That’s the proverbial tail wagging the dog. Instead, you should buy property if you’ve identified the ideal home, can afford the payments, have run various scenario analysis, and plan to live or own the home for years to come.

My lender said the demand he is seeing for purchase applications is the strongest he’s seen all year. Business is booming because refinancing continues to be super strong as well. The key question is whether the banking industry will return to its pre-pandemic lending standards sooner, rather than later.

If it does, it would mean that the labor market has returned and liquidity and profitability fears have dissipated. As a result, property prices will continue to march higher.

There is certainly a scenario where we could see the “mother of all bidding wars” in the second half of the year and beyond given there are months of pent-up demand. The stock market is certainly anticipating such an economic recovery.

However, if things don’t get better, then any property buyer today will likely have to ride out the storm for at least two or three years. Hopefully, most buyers will be OK since the average ownership duration is over nine years. However, as always, some people are going to get hurt at the margin.

Please really think things through before purchasing a property today. Yes, mortgage rates are enticingly low. Yes, open houses are not back yet, which means you don’t have to get into a bidding war with emotional buyers. However, I encourage you to take your time.

If you haven’t found the ideal property, move on. There will always be another property that will come along. Finally, pay attention to your local mortgage industry. The supply of capital is paramount for a strong housing market.

Readers, what has your experience been with getting a conforming mortgage and a jumbo mortgage in this environment? How is the mortgage industry and real estate market where you live? If the demand for real estate is high where you live, why do you think that is? Where do you see weakness in real estate?