According to the Energy Information Administration, US petroleum inventories (excluding SPR) dropped by 2.6 million barrels last week to 1.444 billion, whereas SPR stocks dropped by 1.6 million barrels. Total stocks stand 152 mmb above the rising, rolling 5-year average and about 133 mmb higher than a year ago. Comparing total inventories to the pre-glut average (end-2014), stocks are 385 mmb above that average.

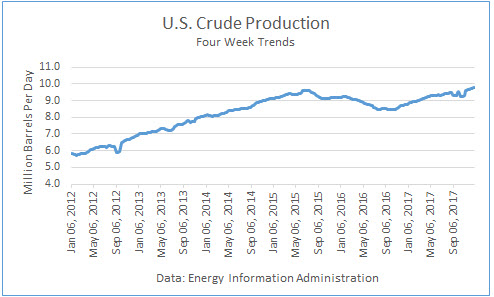

Crude Production

Production averaged 10.7 mmbd last week, down unchanged from the prior week, and 10.875 mmbd over the past 4 weeks, off 11.4 % v. a year ago. In the year-to-date, crude production averaged 11.974 mmbd, off 1.1 % v. last year, over 200,000 b/d lower.

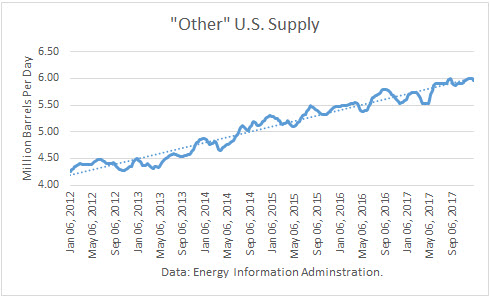

Other Supply

I have previously noted in an article how the “Other Supply,” primarily natural gas liquids and renewables, are integral to petroleum supply. The EIA reported that it dipped 3,000 b/d v. last week at 6.639 mmbd. The 4-week trend in “Other Supply” averaged 6.746 mmbd, off 6.7 % over the same weeks last year. In YTD, they are unchanged from 2019.

Crude production plus other supplies averaged 17.621 mmbd over the past 4 weeks, well below the all-time-high record.

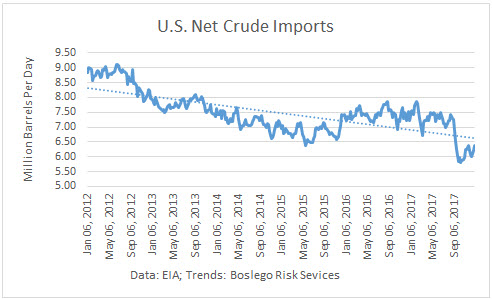

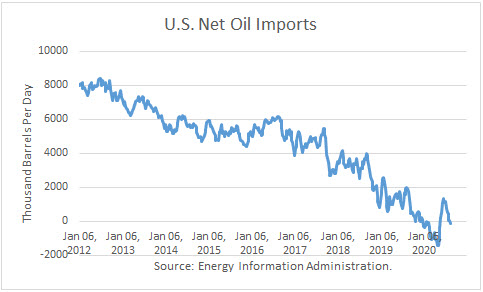

Crude Imports

Total crude imports rose by 109,000 b/d last week to average 5.730 mmbd last week. This figure was above the 4-week trend of 5.627 mmbd, which in turn was off 21.7 % from a year ago.

Net crude imports rose by 1.115 mmb/d because exports fell by 1.006 mmb/d to average 2.137 mmbd. Over the past 4 weeks, crude exports averaged 2.838 mmbd, 14.0 % higher than a year ago.

U.S. crude imports from Saudi Arabia rose by 142,000 last week to average 433,000 b/d. Over the past 4 weeks, Saudi imports have averaged 304,000 b/d, down 25 % from a year ago.

Crude imports from Canada fell by 81,000 b/d last week, averaging 3.358 mmbd. Imports over the past 4 weeks averaged 3.468 mmbd, off 5.4 % v. a year ago.

Net oil exports averaged 111,000 b/d over the past 4 weeks. That compares to net oil imports of 1.938 mmb/d over the same weeks last year.

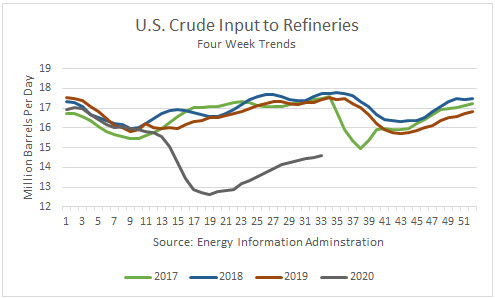

Crude Inputs to Refineries

Inputs fell by 171,000 b/d last week last week averaging 14.487 mmbd. Over the past 4 weeks, crude inputs averaged 14.594 mmbd, off 16.3 % v. a year ago. In the year-to-date, inputs averaged 14.527 mmbd, off 13.0 % v. a year ago.

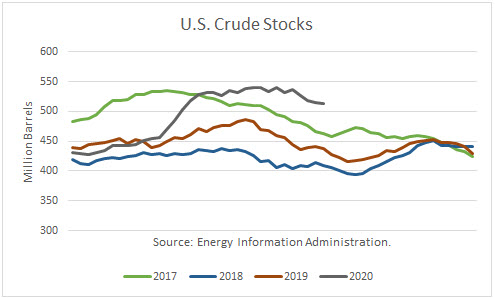

Crude Stocks

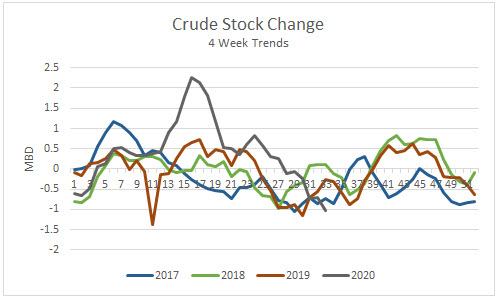

Over the past 4 weeks, crude oil demand exceeded supply by 1.037 mmb/d.

Commercial crude stocks 512.5 mmb are now 74.7 million barrels higher than a year ago.

Petroleum Products

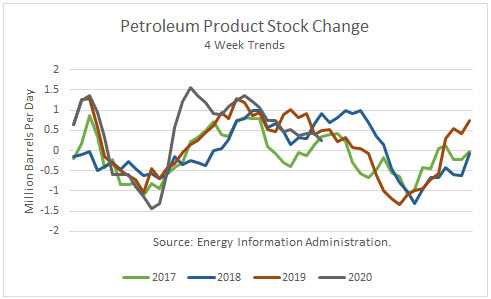

Given the recent net product stock builds, product supply has exceeded demand by 242,000 b/d.

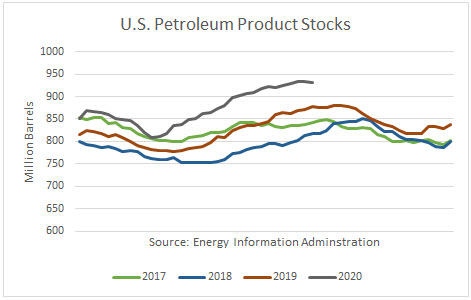

Total U.S. petroleum product stocks at 931 mmb are 61 million barrels higher than a year ago.

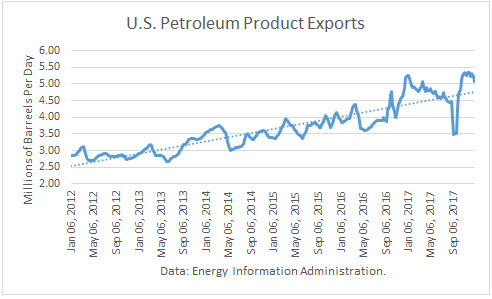

Product exports rose by 991,000 b/d last week, averaging 5.653 mmbd. The 4-week trend of 4.913 mmbd is off 7.4 % from a year ago. In the year-to-date, exports averaged 5.065 mmbd, off 0.5 % from a year ago.

Demand

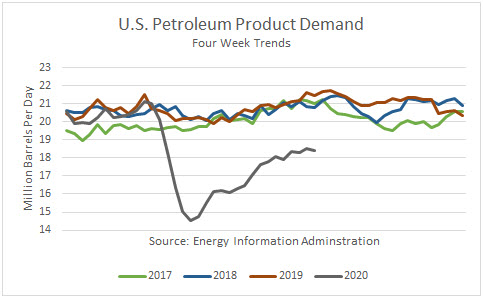

Total petroleum demand averaged 18.384 over the past 4 weeks, off 14.3 % v. last year. In the YTD, product demand averaged 18.119 mmbd, off 12.5 % v. the same period in 2019.

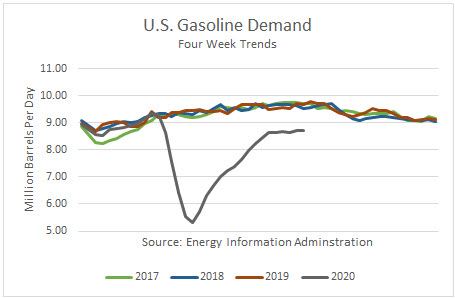

Gasoline demand at the primary stock level fell by 253,000 b/d last week and averaged 8.735 mmbd over the past 4 weeks, off 9.9 % v. the same weeks last year. In the YTD, it reported that gas demand is off 14.4 % v. a year ago.

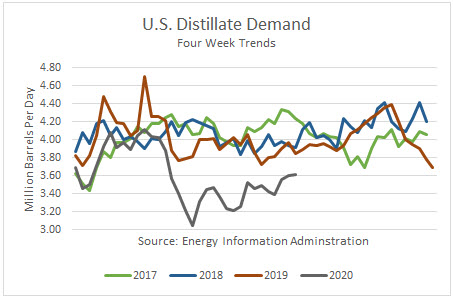

Distillate fuel demand, which includes diesel fuel and heating oil, fell by 610,000 b/d last week, and averaged 3.612 mmbd over the past 4 weeks, off 6.1 % the same weeks last year. In the YTD, demand is off 10.2 % v. a year ago.

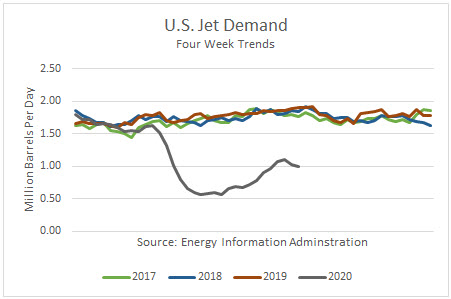

Jet fuel demand is off 47.6 % over the past 4 weeks v. last year. In the year-to-date, demand was off 38.9 % v. 2019.

Product Stocks

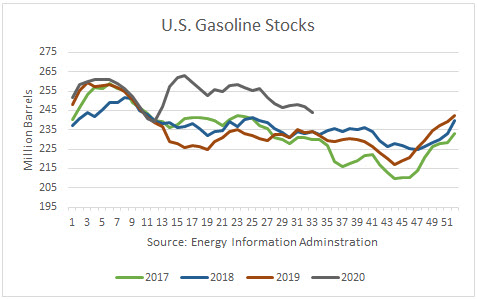

Gasoline stocks are now 9.7 mmb higher than a year ago, ending at 243.8 mmb.

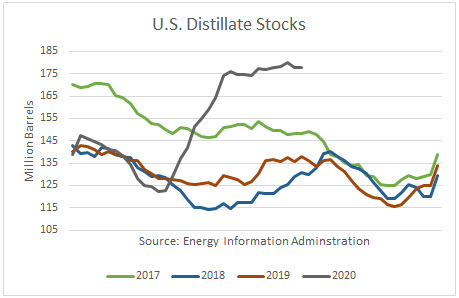

Distillate stocks are 39.7 mmb higher than a year ago, ending at 177.8 mmb.

Conclusions

Crude stocks are dropping faster due to relatively low imports and lower U.S. production. But the surplus stands at 75 million barrels and that will take many months to correct.

Petroleum product demand appears to be leveling off, down almost 15 percent from a year ago. The product surplus is a little smaller than the crude surplus but in total stocks are more than 130 million barrels higher than a year ago.

WTI crude prices have stabilized just above $40/b. Blotted stocks are keeping oil prices from rising further and on-going stock correction is keeping them from falling.

Check back to see my next post!

Best,

Robert Boslego

INO.com Contributor – Energies

Disclosure: This contributor does not own any stocks mentioned in this article. This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.