It’s been a pretty good year so far for mortgage rates, which topped out at around 8% last year.

The 30-year fixed is now priced about one full percentage point below its year ago levels, per Freddie Mac.

And when you consider the high of 7.79% seen in October 2023, is now over 150 basis points lower.

But the recent mortgage rate rally may still have some gas in the tank, especially with how disjointed the mortgage market got in recent years.

Simply getting spreads back to normal could result in another 50 basis points (.50%) or more of relief for mortgage rates going forward.

Forget the Fed, Focus on Spreads

There are a couple of reasons mortgage rates have improved over the past 11 months or so.

For one, 10-year treasury yields have drifted lower thanks to a cooler economy, which is a boost for bonds.

When demand for bonds increases, their price goes up and their yield (interest rate) goes down.

Long-term mortgage rates follow the direction of the 10-year yield because they have similar maturities (mortgages are often prepaid in a decade).

So if you want to track mortgage rates, the 10-year yield is a good place to start.

Anyway, inflation has cooled significantly in recent months thanks to monetary tightening from the Fed.

They raised rates 11 times since early 2022, which seemed to finally do the trick.

This pushed the 10-year yield down from nearly 5% in late October to about 3.65% today. That alone could explain a good chunk of the mortgage rate improvement seen since then.

But there has also been some narrowing of the “spread,” which is the premium MBS investors demand for the risk associated with a home loan vs. a government bond.

Remember, mortgages can fall into default or be prepaid at any time, whereas government bonds are a sure thing.

So consumers pay a premium for a mortgage relative to what that bond might be trading at. Typically, this spread is around 170 basis points above the 10-year yield.

In other words, if the 10-year is 4%, a 30-year fixed might be offered at around 5.75%. Lately, mortgage rate spreads have widened due to increased volatility and uncertainty.

In fact, the spread between the 10-year and 30-year fixed nearly doubled from its longer-term norm, meaning homeowners were stuck with a rate 3%+ higher.

For example, when the 10-year was around 5%, a 30-year fixed was priced around 8%.

Normalizing Spreads Could Drop Rates Another 60 Basis Points

New commentary from J.P. Morgan Economic Research argues that “primary mortgage rates could fall by as much as 60 bps over the next year” thanks to spread normalization alone.

And even more than that if the market prices in more Fed rate cuts.

They note that the primary/secondary spread — what a homeowner pays vs. the secondary mortgage rate (what mortgage-backed securities trade for on the secondary market) remains wide.

Head of Agency MBS Research at J.P. Morgan Nick Maciunas said if the yield curve re-steepens and volatility falls, mortgage rates could ease another 20 bps (0.20%).

In addition, if prepayment risk and duration adjustment fall back in line with their norms, spreads could compress another 20 to 30 bps.

Taken together, Maciunas says mortgage rates could improve another 60 basis points (0.60%).

If we consider the 30-year fixed was hovering around 6.35% when that research was released, the 30-year might fall to 5.75%.

But wait, there’s more. Aside from the mortgage market simply rebalancing itself, additional Fed rate cuts (due to a continued economic slowdown) could push rates even lower.

How Much Will the Fed Actually Cut Over the Next Year?

Remember, the Fed doesn’t set mortgage rates, but it does take cues from economic data.

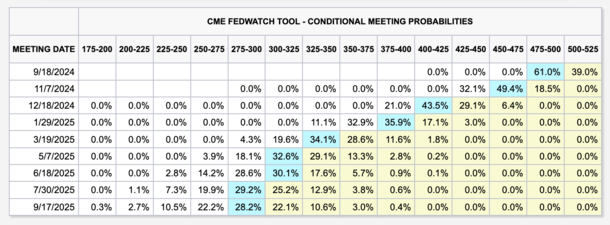

At last glance, the CME FedWatch tool has the fed funds rate hitting a range of 2.75% to 3.00% by September 2025.

That’s 250 bps below current levels, of which some is “priced in” and some is not. There’s still a chance the Fed doesn’t cut that much.

However, if it becomes more apparent that rates are in fact too high and going to drop to those levels, the 10-year yield should continue to fall.

When we combine a lower 10-year yield with tighter spreads, we could see a 30-year fixed in the low 5s or even high 4s next year.

After all, if the 10-year yield slips to around 3% and the spreads return closer to their norm, if even a bit higher, you start to see a 30-year fixed dip below 5%.

Those who pay discount points at those levels might have the chance to go even lower, perhaps mid-to-low 4s and maybe, just maybe, something in the high 3s depending on loan scenario.

Just note this is all hypothetical and subject to change at any given time. Similar to the ride up for mortgage rates, there will be hiccups and unexpected twists and turns along the way.

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 18 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on Twitter for hot takes.